This isn't a minor material shift. The move from steel-heavy conventional vehicles to polymer-intensive EVs represents a fundamental change in how automotive components are specified, sourced, and manufactured. For OEMs, Tier-1 suppliers, and component manufacturers operating in India's rapidly expanding EV market, understanding where plastics fit — and why demand is accelerating — is increasingly a strategic necessity.

Key Takeaways

- India's EV market is growing at roughly 55% CAGR through 2034, creating compounding demand for polymer components across every vehicle subsystem

- Automotive plastics in India are projected to reach ₹18,400+ crore (USD 2,217.7 million) by 2034, with EVs as the primary growth driver

- Battery weight pressure drives OEMs to lightweight every other component, making polymer substitution for metal the default engineering response

- Engineering polymers (PA, PC, ABS) are replacing metals in battery enclosures, connector housings, and structural components

- FAME, PM E-DRIVE, and PLI schemes are amplifying both EV adoption and downstream plastic component demand

Lightweighting: Why EVs Need More Plastics Than Conventional Vehicles

Battery packs are heavy. A typical EV battery system adds 300–600 kg to the vehicle platform compared to a conventional ICE drivetrain. That weight penalty gets distributed across every other component in the vehicle.

This is the core reason plastic demand in EVs structurally outpaces that in ICE vehicles. For EV engineers, lightweighting is a direct tool for recovering range lost to battery mass — not an aesthetic choice.

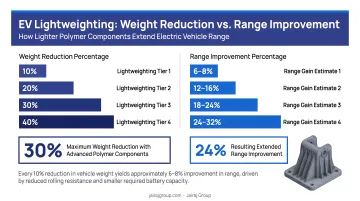

The Weight-Range Relationship

Research published in Science Direct indicates that a 10% reduction in vehicle weight can improve EV energy efficiency by approximately 6–8%, with direct gains in per-charge range. At a component level, replacing a steel bracket or panel with a glass-fiber reinforced polymer equivalent can reduce component weight by 40–60% without compromising structural performance.

These numbers compound quickly across a full vehicle bill of materials. Replace enough metal with polymer composites across bumpers, door panels, seat structures, and underbody trays, and you're recovering measurable range without any change to battery chemistry or capacity.

What Indian OEMs Are Doing

These efficiency gains are already shaping design decisions among Indian OEMs. Ather Energy's Redux concept scooter, developed in collaboration with Swiss composites firm Bcomp, used flax-fibre composite panels to replace conventional plastic bodywork, cutting weight while maintaining structural rigidity. While a concept vehicle, it signals the direction Indian two-wheeler EV manufacturers are moving: bio-composites and engineered fibre-reinforced polymers are entering serious design consideration.

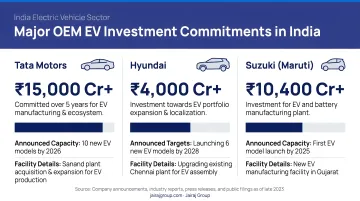

Tata Motors, which has committed ₹16,000–18,000 crore to its EV division through FY30, has consistently referenced lightweight materials as central to its multi-platform EV architecture strategy. As OEM investment scales up, so does the re-engineering of component specs away from conventional steel and aluminium.

Growing Plastic Applications Across India's EV Value Chain

Polymers in EVs are no longer limited to dashboards and bumper fascias. They now serve load-bearing, electrically critical, and thermally demanding roles across multiple vehicle subsystems.

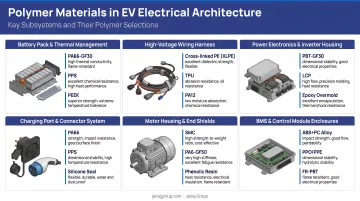

Battery and Energy Storage Systems

Battery module housings and battery management unit (BMU) enclosures require materials that combine thermal stability with electrical insulation — a dual requirement that engineering polymers handle better than most alternatives.

Polyamide (PA66) and polycarbonate blends are the materials of choice here. Each brings specific performance properties:

- PA66: Maintains structural integrity at 150–180°C, resists automotive fluids, delivers dimensional stability for tight-tolerance enclosures

- PC blends: Add impact resistance and flame retardancy relevant to high-voltage environments

- PBT: Used where combined stiffness, chemical resistance, and electrical insulation are needed simultaneously

Meeting these specifications requires more than material selection — it demands tight process control. Jairaj Group's multi-cavity and insert molding capabilities in PA66-GF, PC, and PBT serve this component category directly, with ISO 9001:2015-certified manufacturing and full material traceability to satisfy OEM documentation requirements for battery-adjacent parts.

Electrical and Wiring Architecture

EVs carry significantly more complex electrical architectures than ICE vehicles. A conventional car might have 1,500–2,000 electrical signals; a modern EV can exceed 3,000. That complexity translates directly into more wiring, more connectors, and more polymer material per vehicle.

Key polymer materials in EV electrical systems include:

- PVC: Dominant in low-voltage wiring for cost and flexibility

- XLPE (cross-linked polyethylene): Preferred for high-voltage cables due to superior thermal and dielectric performance

- TPU/TPE: Standard for connector housings where flexibility and chemical resistance are critical

Exterior and Structural Components

Polypropylene dominates bumper systems, wheel arch liners, and underbody panels. ABS composites handle body side cladding and aerodynamic trays. The design advantage of polymers here isn't just weight — it's geometry. Complex aerodynamic profiles that would require expensive multi-piece metal stamping can be produced as single-shot injection molded parts.

Jairaj Group manufactures front bumpers, fenders, and exterior panels using PP, ABS, and PC/ABS blends across automotive OEM programs, with tooling developed in-house and production certified to ISO 9001:2015.

Interior Components and Thermal Management

ABS/PC blends are the standard material for dashboard panels, instrument cluster housings, and infotainment bezels — offering UV resistance, dimensional stability, and surface finish quality simultaneously. These same material combinations apply across door trims, pillar trims, and glove box housings.

The less visible application is thermal management. Specialty polymers — including high-temperature PA and PPS grades — are replacing metal in coolant manifolds, heat shields, and battery thermal management conduits, where weight reduction and corrosion resistance outweigh any thermal conductivity trade-off.

Engineering Polymers Replacing Metals in Critical EV Systems

Not all plastics are equal. Commodity polymers like general-purpose polypropylene or HDPE serve volume applications well, but they can't handle the thermal loads, dimensional precision, or electrical demands of EV powertrain-adjacent systems. Engineering polymers fill that gap — and OEM qualification requirements for EVs are driving adoption faster than anything the ICE era demanded.

Polyamide (PA6 and PA66)

PA grades are the workhorses of metal replacement in under-hood and powertrain applications. PA66 with glass fiber reinforcement delivers tensile strength of 180–220 MPa depending on fill percentage, heat deflection temperatures above 250°C, and chemical resistance to automotive fluids and battery electrolytes.

In EVs specifically, PA finds application in:

- Connector housings and charge port components

- Motor casings and inverter covers

- Coolant manifolds and fluid handling components

- High-voltage junction box enclosures

BASF's Ultramid polyamide grades are validated for EV under-hood coolant exposure, with projected service lives exceeding 100,000 hours — a key reference point for OEM qualification.

Polycarbonate and PC/ABS Blends

Where PA handles thermal and structural loads, polycarbonate addresses optical and safety requirements. PC's combination of clarity, impact resistance, and UL94 V-0 flame retardancy makes it the default choice for EV lighting systems. LED headlamp lenses, high-voltage component covers, and display panels are increasingly produced in polycarbonate — and the global automotive lighting market's shift to PC is well established, with suppliers like Covestro and SABIC citing EV lighting as a primary growth application.

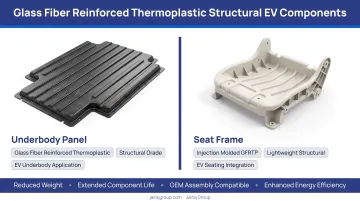

Glass-Fiber and Carbon-Fiber Reinforced Thermoplastics

GFRP and CFRP thermoplastics represent the premium segment of EV structural applications, offering near-metal stiffness at 30–50% lower weight. Early structural targets include:

- Floor structures and underbody panels

- Battery casing frames

- Seat back panels and cross-car beams

Volumes remain modest relative to commodity polymers. As EV platforms move from first-generation architectures to purpose-built designs, cost-per-part economics for reinforced thermoplastics improve — and adoption follows.

What's Driving Plastic Demand in India's EV Ecosystem

Policy and Regulatory Environment

India has built one of the more structured EV policy frameworks among major auto markets:

- FAME Phase II provided ₹10,000 crore in demand-side incentives for EV adoption

- PM E-DRIVE, a ₹10,900 crore scheme announced in 2024, targets charging infrastructure and fleet electrification

- PLI for Automobiles and Auto Components directly incentivises manufacturers investing in advanced EV component production, including polymer-based systems

- BS-VI emissions norms push OEMs toward lightweighting to meet efficiency targets across their fleet

- Customs duty exemptions on lithium, cobalt, and critical minerals signal sustained government commitment to the EV transition

The PLI scheme's structure is particularly relevant for plastic component manufacturers: it rewards domestic production of advanced auto components, which include engineered polymer parts for EV platforms.

OEM Investment Scale

The investment commitments from major OEMs make the demand signal concrete:

- Tata Motors: ₹16,000–18,000 crore committed to EV development through FY30

- Hyundai: USD 2.45 billion invested in Tamil Nadu for EV production over 10 years

- Suzuki Motor: USD 8 billion India investment, with EV production already underway at Gujarat

Every EV platform these OEMs launch creates downstream demand for thousands of polymer components per vehicle.

Supply Chain Localisation

India's Phased Manufacturing Programme (PMP) norms push EV manufacturers toward increasing domestic content over time. As OEM investment scales up, this creates a direct opening for local plastic component suppliers: qualified partners with proximity to assembly plants and the quality systems to support just-in-time schedules.

Suppliers with multi-plant footprints near major OEM clusters — covering NCR, Pune/Aurangabad, Gujarat, and Uttarakhand — are structurally advantaged here. Jairaj Group's facilities in Haryana (Faridabad and Manesar), Gujarat (Sanand), Maharashtra (Aurangabad), and Uttarakhand (Rudrapur) sit directly within the automotive manufacturing clusters where EV investment is concentrating.

Market Outlook and Future Signals for Plastics in India's EV Ecosystem

Market Size Trajectory

According to IMARC Group, India's automotive plastics market was valued at USD 1,507.9 million in 2025 and is projected to reach USD 2,217.7 million by 2034, growing at a 4.25% CAGR. That baseline, however, understates the EV-specific opportunity.

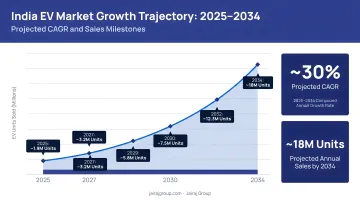

India's EV market itself is growing at approximately 55% CAGR through 2034, from USD 3.71 billion in 2025 toward a projected USD 191 billion — with the government targeting 30% EV share of total vehicle sales by 2030. FY25 EV sales crossed 2.05 million units, up 15.6% year-on-year. As EVs take a larger share of vehicle production, the polymer content per vehicle rises: plastics demand grows faster than the automotive market overall.

Emerging Material and Technology Signals

Three developments will shape polymer demand over the next 2–4 years:

- Bio-based and recycled-content polymers: ESG mandates from global OEMs (already visible in Hyundai and Mercedes-Benz supply chain requirements) will reach Indian EV specifications. Suppliers with recycled-content traceability gain a clear qualification edge

- Multi-material overmolding: EV components increasingly combine rigid polymer structures with soft-touch or conductive overmold layers, requiring both tooling sophistication and multi-material process expertise

- Solid-state battery formats: Solid-state cells entering commercial production (likely post-2027) will shift thermal management requirements. Different operating temperature profiles from liquid electrolyte cells could open specialty polymer applications in cell packaging and thermal interface materials

Positioning for Suppliers

The suppliers best placed to capture growing EV platform programs share a common profile: engineering polymer expertise, precision injection molding capability, multi-plant proximity to OEM clusters, and established quality systems that meet automotive-grade requirements.

Jairaj Group fits squarely within this profile. Its 2023 expansion into EV-focused polymer components is backed by ISO 9001:2015 certification, in-house tool room capabilities, and a manufacturing network spanning Haryana, Gujarat, Maharashtra, Uttarakhand, and Gurugram. The company currently produces EV charger handles, fan grills for EV charging systems, and battery covers, with broader capabilities in PA66-GF, PC/ABS, and engineering polymer processing applicable across EV battery, electrical, exterior, and interior component categories.

Frequently Asked Questions

What is the growth of the electric vehicle industry in India?

India's EV market was valued at approximately USD 3.71 billion in 2025 and is projected to reach USD 191 billion by 2034 at roughly 55% CAGR. FY25 saw 2.05 million EV units sold, up 15.6% year-on-year, with India targeting 30% EV share of total vehicle sales by 2030.

Which plastic materials are most commonly used in electric vehicles?

The most widely used polymers in EVs include:

- Polypropylene (PP) — structural and exterior components

- Polyamide/PA — under-hood parts and connectors

- Polycarbonate (PC) — lighting and display systems

- ABS — interior trim and panels

- PVC — low-voltage wiring

- Polyurethane (PU) — seating and insulation

How do plastics help improve the range of electric vehicles?

Replacing heavier metals with lightweight polymers reduces overall vehicle curb weight. Since EVs consume energy proportional to the mass they move, lower weight means less energy consumed per kilometre — directly extending the range achievable on a single battery charge.

What is the market size of automotive plastics in India?

India's automotive plastics market stood at USD 1,507.9 million in 2025 and is projected to reach USD 2,217.7 million by 2034 at a 4.25% CAGR, according to IMARC Group. EV platform growth is a primary demand driver within this market.

What role does government policy play in driving plastic adoption in Indian EVs?

FAME, PM E-DRIVE, and PLI for auto components incentivise EV manufacturing at scale, which directly increases demand for EV-grade polymer components. BS-VI emissions norms also push OEMs toward lightweighting strategies, where polymer substitution is a primary lever.

How is the rise of EVs affecting plastic component manufacturers in India?

EV growth expands the addressable market for polymer component suppliers, particularly those with engineering plastics expertise and precision injection molding capabilities. OEMs are actively seeking quality-certified, locally based suppliers for battery enclosures, electrical components, and structural parts as domestic content requirements tighten.