The margin pressure is real. ABC Technologies, one of North America's largest automotive plastic systems suppliers, saw Adjusted EBITDA margin collapse from 12.1% in FY2021 to 4.2% in FY2022 — citing resin inflation, freight costs, and OEM shutdowns as primary drivers. Squeezing unit prices didn't save them. The cost was already locked in upstream.

That's the central problem this blog addresses. Value engineering (VE) for automotive plastic components isn't purely a design exercise, and it's not purely a procurement exercise. It operates at the intersection of both — through decisions made in design, supplier selection, process matching, and supply chain structure. Getting any one of these wrong compounds costs across the rest.

Key Takeaways

- Plastics represent roughly ₹38,000+ in material value per vehicle — enough to move margins significantly when managed well or poorly

- A large portion of component cost is locked in before production begins, making early supplier involvement the single highest-impact VE opportunity available

- The main cost drivers: over-specification, process mismatches, tooling mismanagement, and supplier fragmentation

- Effective VE works across three levels: design decisions, supply chain execution, and structural programme governance

- Sustainable cost reduction requires VE to be continuous and cross-functional, not a one-time launch activity

How Supply Chain Costs Around Automotive Plastic Components Build Up

Plastic component supply chain costs rarely appear as a single visible line item. They build up across rejected parts, excess tooling spend, unplanned re-tooling, redundant inventory, and premium freight that only surfaces under volume or schedule stress.

The real problem is how these costs compound. A misspecified material grade doesn't just raise raw material cost — it triggers downstream testing cycles, supplier requalification runs, and production delays that can triple the original decision's cost. By the time procurement sees the damage, fixing it costs far more than preventing it would have.

Most procurement teams track unit price. What they miss:

- Scrap rates and first-pass yield trends

- Tooling downtime from unmanaged cavity wear

- Inventory tied up to buffer supplier unpredictability

- Revalidation cost when specs change mid-program

- Freight premiums from reactive expediting

The gap between visible cost and total cost is where margin disappears — and where effective value engineering focuses its effort.

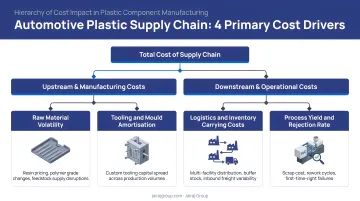

Key Cost Drivers Across the Automotive Plastic Supply Chain

Cost in automotive plastic supply chains is shaped by four primary forces:

- Design decisions — geometry, tolerances, and material grades locked in early

- Process selection — which molding technology is chosen, and whether it matches the design

- Supplier capability fit — whether the supplier's equipment, tooling, and quality systems match the part's actual requirements

- Supply chain structure — single vs. multi-source, nearshore vs. offshore, transactional vs. partnership-based

Of these four, design decisions create the longest shadow. Here's why.

Why Early Decisions Carry the Heaviest Cost Consequences

MIT Sloan research found that 70% to 90% of manufacturing cost is determined by product design — with the exact share varying by product type. For injection-molded plastic components, the mechanism is direct: geometry and material choices determine wall thickness, rib design, gate strategy, and cavity count. Cycle time and scrap risk follow from those same decisions, all before a single shot is pulled.

An academic cost model built on 75 injection mold tooling quotes confirmed that part size, dimensional complexity, actuators, surface finish, and tolerance levels are the primary statistical drivers of both mold cost and lead time. These are all design-stage variables.

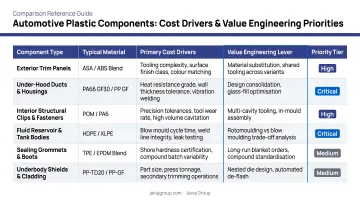

How Cost Drivers Shift by Component Type

Not all plastic parts carry the same risk profile:

| Component Type | Dominant Cost Driver | VE Priority |

|---|---|---|

| High-volume commodity parts (clips, brackets) | Material pricing, cycle time | Resin grade rationalization, cavity count |

| Functional precision parts (sealing, NVH) | Scrap rate, process consistency | DfM review, tolerance stack analysis |

| Structural/safety components | Tooling quality, rejection rate | Supplier qualification depth |

| Large hollow parts (ducts, tanks) | Process selection, wall uniformity | Injection vs. blow molding evaluation |

Cost-Reduction Strategies That Actually Work

No single strategy universally reduces cost across all plastic component supply chains. The right lever depends on where cost actually originates — at the decision stage, during active supply chain management, or in the structural setup of the supply base.

Before Tooling Is Committed: Upstream Cost Decisions

These are upstream interventions — made before tooling is committed — where the cost of getting it right is lowest and the payoff is highest.

Early supplier involvement in design

Bringing the component manufacturer into the development phase before tool release allows a function-based review of tolerances, wall thickness, gate placement, and material grades. This is where DfM reviews catch the problems that become expensive after tooling sign-off.

Jairaj Group's Value Engineering Centers operate at this stage, conducting flow analysis, cooling optimization, warpage prediction, and process simulations before tooling is authorized. Their R&D teams work with customers to convert end-use requirements into manufacturable, cost-effective designs from the first iteration — not after tooling rework forces a redesign.

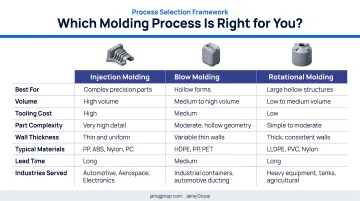

Process-to-design matching

Using injection molding for a large hollow component better suited to blow molding inflates both tooling investment and cycle time. The reverse is equally costly. VE studies that evaluate process fit before tooling sign-off eliminate this risk — and the savings are structural, not recoverable through unit price negotiation later.

Jairaj's process selection framework maps component requirements to the right technology:

- Injection molding for tight-tolerance functional components

- Blow molding for lightweight hollow parts requiring structural uniformity

- Rotational molding for large seamless enclosures where weld-line-free integrity matters

Material grade rationalization

Over-specifying polymer grades — using PA66-GF where standard PP meets functional requirements — is one of the most common and correctable cost errors in automotive plastics. The ACC automotive plastics roadmap identifies polymer grade consolidation as a platform-level cost and recyclability priority.

The discipline required is function analysis, not materials substitution. Each premium resin should be tied to a documented heat, chemical, UV, impact, or dimensional requirement. Without that gate, engineering-grade specifications tend to persist through inertia rather than necessity.

Part consolidation

Reducing component count through design-for-assembly — combining two injection-molded parts into one blow-molded or over-molded unit — reduces tooling count, assembly labor, fastener cost, and supplier coordination overhead. The trade-off is real: consolidated tools can raise complexity, cavity balance risk, and repair cost. That trade-off needs to be modeled before committing to a single large integrated tool rather than assumed away.

During Active Production: Supply Chain Discipline

Once tooling is committed, cost management shifts to process discipline and supplier accountability. These strategies don't require eliminating vendors — they require better visibility into what's actually happening on the floor.

Supplier quality metrics as a cost lever

Rejection rates, rework frequencies, and first-pass yield data are more powerful cost indicators than unit price. A supplier quoting 8% below market but running a 4% scrap rate almost certainly costs more in total.

OEM supplier scorecards should surface:

- First-pass yield by part number and cavity

- Rework frequency and the root causes driving it (tooling, process, or material)

- Unplanned downtime attributed to tooling vs. process vs. material

- Dimensional compliance trends across batches

Tooling lifecycle management

Unplanned tool maintenance and mid-production re-tooling are significant hidden costs — both in direct spend and in the PPAP revalidation work that follows. Proactive tracking of tool shot counts, cavity wear patterns, and scheduled maintenance intervals prevents reactive spend before it compounds into production disruptions.

Inventory reduction through cycle time consistency

Safety stock requirements often reflect supplier process unpredictability more than actual demand variation. When a supplier's cycle time is inconsistent — driven by uncontrolled process variables rather than demand — OEMs build buffer inventory to compensate. Jairaj's use of PLC-controlled machinery with real-time cavity pressure monitoring and automated cooling sequences directly targets this: consistent process output reduces the unpredictability that forces safety stock in the first place.

Structural Changes: Longer-Term, More Durable Impact

The strategies above operate within an existing supply chain structure. These go further — reshaping who the supply base is, where it's located, and what it's capable of developing.

Supplier consolidation into strategic partnerships

Fragmenting plastic component sourcing across many vendors creates coordination overhead, reduces tooling investment leverage, and limits the depth of supplier-side VE capability. The Deloitte 2023 Automotive Supplier Study noted that OEMs are actively engineering complexity out of vehicles — which creates fewer but more competitive supplier opportunities, favoring suppliers capable of engaging across the full program development cycle, not just quoting on released drawings.

Jairaj Group's awards from Tenneco Automotive for "Strategic Business Partner & Customer Centric Collaboration" and from Endurance Technologies for "Best Supplier Award For Fastest & First Time Right Developments" reflect what joint cost reduction roadmaps look like in practice: structured engagement across program development cycles, not one-off pricing pressure.

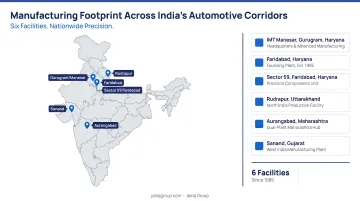

Multi-facility supply base for resilience and logistics efficiency

McKinsey's Supply Chain 4.0 research estimates that advanced supply chain practices can reduce transport and warehousing costs by up to 30%. Geographic proximity to OEM plants matters — it reduces freight cost, buffer inventory requirements, and single-point-of-failure exposure simultaneously.

Jairaj Group's six manufacturing facilities — Faridabad, Rudrapur, Aurangabad, Manesar, Sanand, and Sector 59 — are positioned across India's primary automotive manufacturing corridors. For Indian OEMs managing multi-plant production schedules, this geographic distribution reduces the logistics exposure that a single-source supplier model creates.

Proactive EV and new-platform qualification

EV platforms are creating new plastic component requirements that don't map cleanly onto ICE-era specifications. S&P Global Mobility data shows that thermal management systems in EVs carry 83% higher monetary value content than their ICE equivalents — a direct function of battery cooling complexity. Thermoplastic battery enclosures are emerging as alternatives to aluminum and steel solutions, driven by weight and cost pressure.

OEMs that begin VE work on these components during platform development — not after SOP — avoid the premium cost of reactive re-engineering. Jairaj's expansion into EV-focused polymer components and development of EV charger components positions them for early-stage engagement on these new platform requirements.

Conclusion

Cost reduction in automotive plastic supply chains doesn't come from squeezing unit prices. It comes from correctly diagnosing where cost originates — whether that's a design decision locked in too early, a process gap accumulating quietly during production, or a structural supply chain problem that procurement pressure alone won't resolve — and applying the right lever at the right stage.

Effective value engineering isn't a one-time event at product launch. It's a continuous discipline embedded into supplier partnerships, engineering reviews, and supply chain governance.

Manufacturers who build this into their process — structured DfM reviews before tooling sign-off, proactive tooling lifecycle management, supplier relationships built around joint cost reduction — consistently outperform on margin, quality, and delivery. Those who treat it as a periodic cost-cutting exercise find the savings don't hold.

Frequently Asked Questions

What is value engineering in the automotive industry?

Value engineering in automotive is a systematic process of analysing product functions against cost to improve performance while eliminating unnecessary spend. It applies at both design and production stages, with the goal of improving the value ratio — more function for lower cost — rather than simply cutting costs.

What are the components of value engineering?

The core steps are information gathering, function analysis, idea generation, evaluation of alternatives, development of solutions, and implementation. For automotive plastic supply chains, function analysis and idea generation are where the highest-impact decisions are made — particularly around material grades, tolerances, and process selection.

What is the difference between value analysis and value engineering?

Value engineering applies during design and development of new products, before production begins. Value analysis is applied to existing products already in production. Both share the goal of maximising function relative to cost, but acting early costs far less than retrofitting changes after production begins.

How does early supplier involvement reduce costs for plastic components?

Early involvement lets the supplier's engineering team review geometry, tolerances, and material specifications before tooling is committed. Problems at this stage — over-specified wall thickness, poor gate placement, unnecessary surface finish requirements — are inexpensive to fix. After tooling sign-off, the same changes can cost multiples of the original tooling investment.

What role does process selection play in value engineering for automotive plastics?

Matching the manufacturing process to a part's geometry and functional requirements is a core VE decision. Process mismatches inflate tooling cost, cycle time, and scrap rates — and those penalties compound across a program's full life. Using injection molding for large hollow parts, or rotational molding for tight-tolerance components, are common examples.

How should OEMs structure supplier partnerships to support value engineering?

Deep, long-term partnerships outperform transactional sourcing models. Suppliers who participate in design reviews, share tooling investment, and work against joint cost reduction targets deliver more sustained value. The governance mechanism matters: structured engineering reviews and shared quality metrics keep VE continuous rather than episodic.